Financial reporting is the backbone of business transparency and decision-making. Even with professional financial reporting services, businesses can make errors that affect accuracy and compliance. In this blog, we’ll explore the most common mistakes in financial reporting and share practical tips on how to avoid them.

Compliance with regulatory bodies like the IRS and SEC.

Clear communication to investors and stakeholders.

Reliable data for strategic business decisions.

Preparation for audits and financial reviews.

Mistakes in financial reporting can lead to penalties, loss of trust, and poor business outcomes.

Common Financial Reporting Mistakes

1. Incomplete or Missing Data

Failing to record all financial transactions or losing receipts can cause inaccuracies. Every invoice, payment, and expense must be documented.

How to Avoid: Use automated accounting systems and maintain organized records. Partner with financial reporting services that offer data validation and reconciliation.

2. Incorrect Categorization of Expenses and Income

Misclassifying expenses or revenues can distort financial statements and tax filings.

How to Avoid: Follow a consistent chart of accounts standards. Financial reporting services often help with correct categorization based on GAAP.

3. Ignoring Reconciliations

Bank and ledger reconciliations are critical to confirm that financial records match bank statements.

How to Avoid: Schedule monthly reconciliations and use software that flags discrepancies.

4. Failure to Update Financial Reports Regularly

Waiting until year-end to prepare financial reports increases errors and tax risks.

How to Avoid: Update financial reports monthly or quarterly to maintain accuracy and reduce last-minute pressure.

5. Non-Compliance with Financial Reporting Standards

Ignoring GAAP or other relevant standards can lead to unreliable reports and legal issues.

How to Avoid: Ensure your financial reporting services provider is well-versed in GAAP and IRS compliance.

6. Overlooking Disclosure Requirements

Failing to disclose contingent liabilities, accounting policies, or related-party transactions can mislead stakeholders.

How to Avoid: Follow regulatory guidelines closely and consult with experts for proper disclosures.

7. Lack of Internal Controls

Weak controls increase the risk of fraud and errors in financial data.

How to Avoid: Implement segregation of duties, approval workflows, and periodic audits.

How Financial Reporting Services Help Minimize Mistakes

Professional financial reporting services provide:

Expertise to ensure compliance with accounting standards.

Automated tools to reduce human error.

Regular audits and checks to catch discrepancies early.

Training and support to keep your team informed.

Customizable reporting to match your business needs.

The Impact of Technology in Reducing Reporting Errors

Detect anomalies and flag suspicious transactions.

Auto-categorize income and expenses.

Provide real-time updates and alerts.

Simplify bank reconciliations.

Maintain secure audit trails.

Combining professional services with advanced software is the best way to avoid reporting pitfalls.

Summary: Prioritize Accuracy by Avoiding Financial Reporting Mistakes

At Smart Accountants, we understand that avoiding common mistakes in financial reporting safeguards your business’s reputation, compliance, and financial health. Leveraging our expert financial reporting services combined with the right technology ensures your reports are accurate, timely, and trustworthy.

FAQs About Financial Reporting Mistakes

Q1: What is the most common financial reporting error? Incomplete data and incorrect expense categorization are among the top errors.

Q2: How often should financial reconciliations be done? Monthly reconciliations are recommended to maintain accuracy.

Q3: Can small businesses avoid these mistakes without professional help? While possible, professional services greatly reduce risk and errors.

Q4: Does automation replace the need for financial reporting services? Automation helps but expert oversight remains essential.

Q5: How can I train my team to avoid reporting mistakes? Regular training, clear processes, and using reliable services are key.

In today’s fast-paced business environment, accurate and timely financial reporting is crucial. Financial reporting software has revolutionized how companies prepare, analyze, and share their financial data. For businesses in the USA seeking reliable financial reporting services, selecting the right software is key to success in 2025 and beyond.

What is Financial Reporting Software?

Financial reporting software refers to specialized applications designed to automate the process of creating financial statements and reports. These tools help businesses collect financial data, generate reports compliant with financial reporting standards like GAAP, and provide actionable insights.

Modern software solutions offer features such as:

Automated report generation

Integration with accounting systems (e.g., QuickBooks, Xero)

Real-time dashboards

Data visualization

Compliance checks

Cloud access for collaboration

Using financial reporting software enhances accuracy, saves time, and reduces the risk of human error.

Why Is Financial Reporting Software Important for Businesses?

1. Improved Accuracy and Compliance

Manual reporting is prone to errors. Financial reporting software enforces rules based on GAAP or IFRS, ensuring your reports meet all regulatory standards. This compliance is vital to avoid penalties and maintain stakeholder trust.

2. Time and Cost Efficiency

Automation cuts down the hours spent on data entry and report formatting. Your finance team can focus on analysis and strategic planning rather than manual report creation, leading to cost savings.

3. Real-Time Insights for Better Decisions

Many platforms provide live dashboards and customizable reports, enabling business leaders to monitor financial health and make informed decisions promptly.

4. Simplified Audit Processes

Software with audit trails and documentation makes preparing for audits smoother and less stressful.

Top Financial Reporting Software Tools for US Businesses in 2025

Here’s an overview of some leading tools that integrate well with financial reporting services:

1. QuickBooks Online Advanced

Designed for small to mid-sized businesses.

Offers customizable financial reports.

Integrates easily with payroll and inventory management.

Cloud-based with multi-user access.

2. Xero

Cloud accounting platform with strong reporting features.

Real-time dashboards and collaboration tools.

Supports multiple currencies for international businesses.

Easy bank feeds and reconciliations.

3. Sage Intacct

Best suited for mid to large businesses.

Robust reporting and compliance features.

Advanced automation and financial consolidation.

Scalable cloud platform with strong API integrations.

Business Size & Complexity: Small businesses may prefer QuickBooks or Xero, while larger firms might need Sage Intacct or Oracle NetSuite.

Integration Capabilities: Ensure the software connects with your current accounting and ERP systems.

Compliance Features: Look for automatic GAAP or IFRS compliance checks.

User Friendliness: Choose software with an intuitive interface to minimize training time.

Customization: The ability to create reports tailored to your business needs is essential.

Cloud vs On-Premises: Cloud solutions offer flexibility and remote access, while on-premises may suit businesses with strict data control needs.

Customer Support & Training: Strong vendor support and resources help smooth adoption.

The Role of Financial Reporting Services in Software Implementation

Implementing financial reporting software often requires expertise beyond installation:

Data Migration: Safely transferring historical data without loss.

System Configuration: Tailoring the software settings for your business requirements.

Training: Helping your team get up to speed quickly.

Ongoing Support: Addressing issues and updates post-implementation.

Reporting Strategy: Designing the right reports to extract actionable insights.

Partnering with professional financial reporting services providers can ensure smooth implementation and maximize your software investment.

Emerging Trends in Financial Reporting Software for 2025

1. Artificial Intelligence and Machine Learning

AI-driven tools now help detect anomalies, predict cash flow, and automate routine tasks, improving accuracy and foresight.

2. Robotic Process Automation (RPA)

RPA automates repetitive data processing, reducing manual errors and speeding up report generation.

3. Cloud Collaboration

More teams work remotely, and cloud platforms enable real-time collaboration on financial reports regardless of location.

4. Mobile Accessibility

Financial reporting apps optimized for mobile devices allow on-the-go access to critical data and reports.

5. Enhanced Data Security

With cyber threats increasing, software providers are investing heavily in encryption, multi-factor authentication, and compliance with privacy regulations.

Summary: Unlock Efficiency with the Right Financial Reporting Software

Selecting the right financial reporting software is a strategic decision that can transform your business operations. When combined with expert financial reporting services from Smart Accountants, the right software boosts accuracy, compliance, and business insights — all vital for thriving in today’s competitive market.

FAQs About Financial Reporting Software

Q1: Can financial reporting software handle tax compliance? Many tools offer tax-specific reporting and integration with tax software.

Q2: Is cloud-based software secure for financial data? Yes, leading providers follow strict security protocols and compliance.

Q3: How long does it take to implement financial reporting software? Implementation varies from weeks to months, depending on business complexity.

Q4: Do I need expert help to use financial reporting software? While some tools are user-friendly, expert services help optimize usage and reporting quality.

Q5: Can financial reporting software integrate with other business tools? Most modern software supports integrations with payroll, ERP, CRM, and more.

Understanding financial reporting standards is essential for businesses using financial reporting services. In the USA, the most widely followed framework is GAAP (Generally Accepted Accounting Principles). This blog breaks down what GAAP means and why it matters to your business.

What Are Financial Reporting Standards?

Financial reporting standards are the rules and guidelines companies must follow when preparing their financial statements. These standards ensure consistency, transparency, and comparability across businesses.

In the USA, GAAP is the official standard for financial reporting, developed by the Financial Accounting Standards Board (FASB).

What is GAAP?

GAAP stands for Generally Accepted Accounting Principles. It’s a collection of accounting rules, standards, and procedures that companies use to prepare financial statements.

GAAP covers:

Revenue recognition

Balance sheet classification

Expense matching

Disclosure requirements

Measurement of assets and liabilities

Adhering to GAAP ensures your financial reports are accurate, reliable, and accepted by investors, lenders, and regulators.

Why Is GAAP Important for Financial Reporting Services?

Compliance: GAAP compliance is mandatory for publicly traded companies and highly recommended for private businesses.

Trust: GAAP-based reports are trusted by investors and financial institutions.

Comparability: Allows comparison across companies and industries.

If you want to learn how professional financial reporting services ensure GAAP compliance, explore our financial reporting services guide.

What Are Other Financial Reporting Standards?

Though GAAP is dominant in the USA, international businesses often follow IFRS (International Financial Reporting Standards).

Some businesses may also need to consider:

Tax Reporting Standards (IRS specific)

SEC Reporting Requirements for public companies

Industry-Specific Accounting Standards

How Do Financial Reporting Services Help with GAAP Compliance?

Professional financial reporting providers:

Prepare financial statements according to GAAP rules.

Update reports based on the latest GAAP changes.

Use software that enforces GAAP compliance.

Offer expert advice on complex accounting treatments.

Ensure disclosures meet regulatory requirements.

Common GAAP Principles You Should Know

Consistency: Use the same accounting methods over time.

Relevance: Provide useful information for decision-making.

Reliability: Reports must be accurate and verifiable.

Comparability: Financial information should be comparable across periods and companies.

Materiality: Disclose all important information that could influence decisions.

Summary: GAAP — The Foundation of Financial Reporting Services in the USA

At Smart Accountants, we believe that for any business using financial reporting services, understanding GAAP is vital—it guarantees your financial reports are accurate, trustworthy, and compliant with legal standards, enabling better business decisions and smoother audits.

FAQs About GAAP and Financial Reporting

Q1: Are GAAP rules the same for all businesses? No, some rules vary based on business size and industry.

Q2: What happens if my financial reports don’t comply with GAAP? You risk penalties, loss of investor confidence, and audit complications.

Q3: Can small businesses choose not to follow GAAP? Some small private companies have alternatives, but GAAP is generally recommended.

Q4: How often does GAAP change? FASB updates GAAP periodically; staying current is important.

Q5: Do financial reporting services keep up with GAAP updates? Yes, reputable providers monitor and apply all GAAP changes.

Preparing financial reports for tax season is one of the most critical tasks for any business. Accurate financial reporting services ensure you comply with IRS regulations, avoid penalties, and optimize your tax filings.

What Financial Reports Are Needed for Tax Season?

During tax season, businesses typically need:

Profit and Loss Statement — shows revenue and expenses.

Balance Sheet — details assets, liabilities, and equity.

Cash Flow Statement — tracks cash inflows and outflows.

Tax-Specific Reports — such as Schedule C for sole proprietors.

These reports form the basis for your tax return and are often required by accountants or tax professionals.

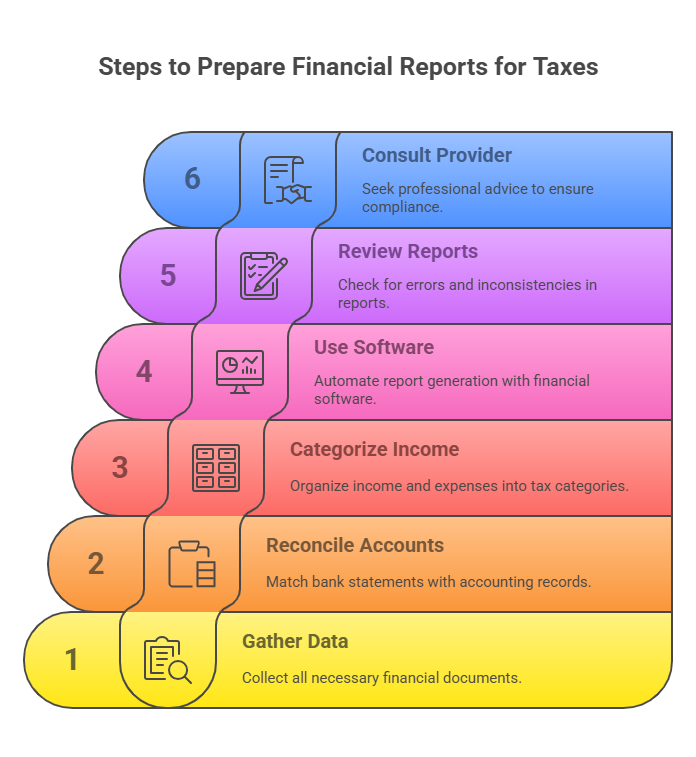

Step-by-Step Guide to Prepare Financial Reports for Taxes

1. Gather All Financial Data Collect invoices, receipts, bank statements, payroll data, and previous tax filings.

2. Reconcile Your Accounts Match bank statements with your accounting records to ensure accuracy.

3. Categorize Income and Expenses Properly Ensure everything is recorded under the correct tax categories to maximize deductions.

4. Use Reliable Financial Reporting Software Automate report generation to reduce human error and save time.

5. Review Reports for Accuracy Check for inconsistencies or missing transactions.

6. Consult Your Financial Reporting Services Provider Professional services can audit and verify your reports to meet tax compliance.

Why Use Professional Financial Reporting Services for Tax Preparation?

Expertise in IRS Requirements: Helps you avoid costly mistakes.

Time-Saving: Focus on running your business while experts handle reporting.

Audit Readiness: Detailed and compliant reports make audits less stressful.

Up-to-Date with Tax Laws: Ensure your reports reflect the latest IRS rules.

Common Mistakes to Avoid When Preparing Tax Financial Reports

Missing receipts or documentation.

Incorrect categorization of expenses.

Failing to reconcile accounts.

Not updating reports before filing.

Ignoring changes in tax laws.

How Often Should You Update Financial Reports During the Year?

It’s best practice to update financial reports monthly or quarterly, not just during tax season. This approach reduces year-end stress and improves decision-making throughout the year.

For a detailed explanation of why frequent reporting matters, visit our Financial Reporting Services Overview.

The Role of Technology in Financial Reporting for Tax Season

Modern financial reporting software offers:

Automated report generation.

Integration with tax software.

Real-time data updates.

Secure cloud access.

Choosing a service provider that uses these technologies ensures smooth tax preparation and compliance.

Summary: Make Tax Season Easier with Accurate Financial Reporting

At Smart Accountants, we understand that accurate financial reports are the backbone of a smooth tax season. Leveraging our professional financial reporting services helps you stay compliant, save time, and avoid costly mistakes.

FAQs About Financial Reports for Tax Season

Q1: Can I prepare financial reports for taxes myself? Yes, but professional services reduce errors and save time.

Q2: What happens if financial reports are inaccurate during tax filing? You risk audits, penalties, and fines.

Q3: How can financial reporting services help during an IRS audit? They provide detailed documentation and support.

Q4: Are there special reports needed for different business types? Yes, reports vary for sole proprietors, LLCs, corporations, etc.

Q5: How soon should I start preparing reports before tax deadlines? Start at least 1-2 months before to allow time for review.

Financial reporting services are professional solutions that help businesses prepare, analyze, and present financial statements and reports. These services ensure that your company’s financial data is accurate, compliant with regulations, and useful for decision-making.

What Does Financial Reporting Mean?

At its core, financial reporting involves creating formal records of a company’s financial activities. These reports include key documents such as:

Income Statement (Profit & Loss)

Balance Sheet (Assets, Liabilities, and Equity)

Cash Flow Statement (Money Inflows and Outflows)

Financial reporting helps stakeholders — including business owners, investors, and regulators — understand the financial health of your company.

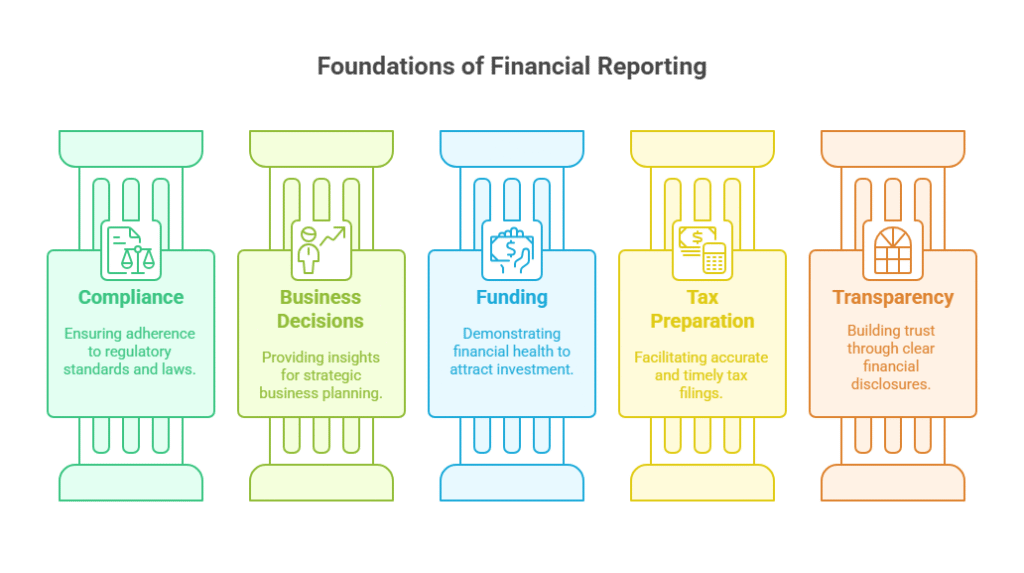

Why Are Financial Reporting Services Important?

Accurate financial reports are essential for:

Compliance: Meeting regulatory requirements like GAAP (Generally Accepted Accounting Principles) or IRS rules.

Business Decisions: Providing actionable insights to improve profitability and growth.

Funding: Demonstrating financial stability to banks, investors, or lenders.

Tax Preparation: Ensuring correct and timely tax filings.

Transparency: Building trust with stakeholders through clear financial disclosure.

What Do Financial Reporting Services Include?

A reliable financial reporting service typically offers:

Preparation of monthly, quarterly, and annual financial statements.

Custom financial reports tailored to your business needs.

Regulatory compliance checks.

Data analysis to identify trends and risks.

Integration with accounting software for automation.

Expert consultation to interpret financial data.

Using financial reporting services frees up time for you to focus on running your business while ensuring your finances are in expert hands.

Who Needs Financial Reporting Services?

Small and Medium Businesses (SMBs): To keep books accurate and reports compliant.

Startups: For investor presentations and financial planning.

Nonprofits: To maintain transparency and fulfill grant requirements.

Corporations: To comply with SEC and other regulatory bodies.

Freelancers & Consultants: To manage income and expenses efficiently.

How to Choose the Right Financial Reporting Services Provider?

Look for a provider that offers:

Expertise in GAAP and IFRS standards.

Experience with your business size and industry.

Use of modern financial reporting software and automation.

Strong customer support and transparent pricing.

Proven track record with positive client testimonials.

Financial Reporting Services and Technology in 2025

Financial reporting is evolving rapidly with the integration of AI and cloud-based platforms. Today’s services often include:

Real-time financial dashboards.

Automated error detection.

Predictive financial analytics.

Secure data storage and easy collaboration.

Partnering with a forward-thinking financial reporting services provider ensures you stay ahead of these trends and maintain a competitive edge.

Summary: Why Invest in Financial Reporting Services?

Investing in professional financial reporting services helps your business:

Stay compliant with evolving regulations.

Make smarter, data-driven decisions.

Save time and reduce errors.

Present transparent and trustworthy financial information to stakeholders.

For any growing business in the USA, the services offered by Smart Accountants are not just a luxury — they’re a necessity.

FAQs About Financial Reporting Services

Q1: What is the difference between bookkeeping and financial reporting services? Bookkeeping records daily transactions, while financial reporting summarizes this data into meaningful reports.

Q2: How often should financial reports be prepared? Typically monthly or quarterly, but some businesses require real-time reporting.

Q3: Are financial reporting services expensive? Costs vary by provider and service complexity; many offer scalable solutions for small businesses.

Q4: Can financial reporting services help with tax audits? Yes, detailed and accurate reports make audit processes smoother.

Q5: Is cloud technology safe for financial reporting? Reputable providers use encrypted cloud platforms that meet strict security standards.