Net income is a crucial financial metric that indicates a company’s profitability after accounting for all expenses, taxes, and costs. Understanding how to calculate net income is essential for business owners, investors, and financial analysts to assess a company’s financial health.

What is Net Income?

Net income, often referred to as the “bottom line,” is the amount of earnings remaining after all expenses have been deducted from total revenue. It reflects the company’s profitability during a specific period and is a key indicator of financial performance. Net income can be positive, indicating profit, or negative, indicating a net loss.

Importance of Net Income in Financial Analysis

Net income serves several vital purposes in financial analysis:

Profitability Assessment: It helps determine how efficiently a company is generating profit relative to its revenue.

Performance Evaluation: Investors and stakeholders use net income to evaluate management’s effectiveness in controlling costs and generating revenue.

Decision Making: Companies rely on net income to make informed decisions regarding expansions, investments, and cost management.

Taxation: Net income is used to calculate tax liabilities, influencing a company’s cash flow and financial planning.

Net Income Formula

The formula to calculate net income is straightforward:

Net Income = Total Revenue – Total Expenses

Breaking it down further:

Net Income = Revenue – Cost of Goods Sold (COGS) – Operating Expenses – Other Expenses – Taxes

Where:

Revenue: Total income from sales or services.

COGS: Direct costs attributable to the production of goods sold by the company.

Operating Expenses: Indirect costs such as salaries, rent, and utilities.

Other Expenses: Includes interest, depreciation, and amortization.

Taxes: Government levies based on earnings.

Calculating Net Income: An Example

Let’s consider a hypothetical company, ABC Widgets, to illustrate the calculation:

Total Revenue: $500,000

COGS: $200,000

Operating Expenses: $150,000

Other Expenses: $30,000

Taxes: $20,000

Applying the formula:

Net Income = $500,000 – $200,000 – $150,000 – $30,000 – $20,000 = $100,000

ABC Widgets has a net income of $100,000 for the period.

Net Income vs. Gross Income

It’s essential to distinguish between net income and gross income:

Gross Income: Calculated as Revenue minus COGS. It represents a company’s profit after deducting the costs associated with making and selling its products but before deducting operating expenses, taxes, and interest. Gross Income = Revenue – COGS

Net Income: Takes gross income and subtracts all other expenses, providing a comprehensive view of profitability.

Example:

Using ABC Widgets’ data:

Gross Income = $500,000 – $200,000 = $300,000

Net Income = $300,000 – $150,000 – $30,000 – $20,000 = $100,000

Net Income and Operating Income

Operating income, also known as operating profit, focuses on earnings from regular business operations, excluding non-operating expenses like taxes and interest. The relationship between net income and operating income is as follows:

Operating Income = Gross Income – Operating Expenses

Net Income = Operating Income – Other Expenses – Taxes

Example:

Continuing with ABC Widgets:

Operating Income = $300,000 – $150,000 = $150,000

Net Income = $150,000 – $30,000 – $20,000 = $100,000

Net Income on the Income Statement

Net income appears at the bottom of the income statement, summarizing the company’s earnings after all expenses. Here’s a simplified representation:

Item

Amount ($)

Revenue

500,000

COGS

(200,000)

Gross Income

300,000

Operating Expenses

(150,000)

Operating Income

150,000

Other Expenses

(30,000)

Taxes

(20,000)

Net Income

100,000

Conclusion

Accurately calculating net income is essential for making informed business decisions, securing investments, and ensuring tax compliance. Whether you are a small business owner or managing a large corporation, understanding net income helps you measure profitability and financial stability.At Smart Accountants, we provide expert accounting services to help businesses streamline their financial operations. Our professional accountancy services cover everything from bookkeeping services to tax planning services, ensuring your financial records are accurate and compliant. Contact us today to learn how we can help you manage your finances effectively!

For small businesses, regulatory compliance can be a daunting and complex challenge. With ever-changing laws, regulations, and standards, businesses must stay vigilant to avoid legal risks, penalties, and operational disruptions. Regulatory compliance encompasses a wide range of obligations, from tax reporting to industry-specific standards, and ensuring compliance is crucial for the smooth operation of any business.

The office clerk regulatory compliance empty form.

In this article, we’ll explore the common regulatory compliance challenges faced by small businesses and provide solutions to help navigate these complexities. We’ll also discuss how integrating accounting services, bookkeeping services, and tax planning services can help small businesses stay compliant and minimize legal risks.

If you’ve previously addressed technology adoption barriers or cash flow management challenges, tackling regulatory compliance should be an equally crucial part of your strategy. Effective compliance management will safeguard your business and support long-term success.

Common Regulatory Compliance Challenges for Small Businesses

Small businesses often face a unique set of regulatory compliance challenges, especially when operating with limited resources or a lack of dedicated legal teams. Let’s take a closer look at the most common challenges that businesses must navigate to stay compliant.

1. Keeping Up with Changing Laws and Regulations

One of the biggest challenges for small businesses is staying up-to-date with the ever-evolving legal landscape. Laws and regulations are constantly changing at the federal, state, and local levels, making it difficult for small businesses to keep track of their compliance requirements.

Impact on the Business: Failure to keep up with changes in laws and regulations can result in fines, penalties, and legal complications. Businesses that miss regulatory updates may also find themselves out of compliance, which can harm their reputation and operations.

2. Navigating Industry-Specific Regulations

Each industry has its own set of regulations and compliance requirements. For instance, businesses in healthcare, finance, or manufacturing face highly specific regulations that govern their operations. Small businesses often struggle to understand and implement these specialized regulations, particularly when they lack legal expertise.

Impact on the Business: Not adhering to industry-specific regulations can lead to severe consequences, including license revocation, penalties, or lawsuits. Small businesses in regulated industries must stay informed about the specific rules governing their sector to avoid costly mistakes.

3. Inadequate Record-Keeping and Documentation

Regulatory compliance often requires businesses to maintain accurate records and documentation, such as tax filings, employee records, and financial statements. Many small businesses fail to implement proper record-keeping systems, which can complicate compliance efforts and expose them to legal risks.

Impact on the Business: Poor record-keeping can lead to missed deadlines, inaccurate filings, and a lack of supporting documentation in the event of an audit. This increases the risk of non-compliance and may result in penalties or legal consequences.

4. Tax Compliance Issues

Tax regulations are a significant aspect of regulatory compliance. Small businesses must navigate complex tax laws, including sales tax, payroll tax, and income tax, and they often lack the resources to manage these requirements effectively. This can result in incorrect tax filings, missed deductions, and tax penalties.

Impact on the Business: Tax compliance issues can result in hefty fines, back taxes, and audits. Without a clear understanding of tax regulations, small businesses may miss opportunities to save money or could face significant financial liabilities.

5. Difficulty Managing Employee Compliance

Businesses must adhere to various labor laws and regulations regarding employee rights, wages, and benefits. For small businesses, staying compliant with these regulations—such as the Fair Labor Standards Act (FLSA), Family and Medical Leave Act (FMLA), and Equal Employment Opportunity (EEO) laws—can be challenging, particularly when resources are limited.

Impact on the Business: Non-compliance with employment laws can lead to lawsuits, fines, and damage to employee morale. Ensuring that employment practices are in line with legal requirements is essential for creating a positive work environment and avoiding costly legal disputes.

6. Balancing Compliance with Operational Efficiency

For many small businesses, balancing compliance with day-to-day operations can be difficult. Compliance-related tasks—such as submitting regulatory filings, conducting employee training, and maintaining financial records—can take time away from running the business. As a result, small business owners may struggle to prioritize compliance without sacrificing operational efficiency.

Impact on the Business: Neglecting compliance due to operational pressures can lead to violations and penalties. Small businesses need to allocate time and resources to ensure that compliance does not interfere with their business’s growth and efficiency.

How to Overcome Regulatory Compliance Challenges

While regulatory compliance can be overwhelming for small businesses, there are practical solutions that can help mitigate these challenges. With the right strategies and tools in place, businesses can stay compliant while maintaining operational efficiency.

1. Stay Informed with Regular Compliance Audits

To keep up with changing regulations, small businesses should implement regular compliance audits. This involves reviewing current practices, policies, and procedures to ensure they align with legal requirements. Audits also provide an opportunity to identify any areas where the business may be falling short in terms of compliance.

Pro Tip: Utilizing accounting services can help streamline the auditing process by ensuring financial records are up to date and accurate. Regular audits will ensure that your business stays compliant with both tax regulations and industry-specific rules.

2. Leverage Industry-Specific Compliance Tools and Resources

For businesses operating in regulated industries, it’s essential to use compliance tools and resources that cater to their specific needs. Industry-specific software or platforms can simplify the process of adhering to regulations, from tracking employee certifications to managing product safety standards.

Pro Tip: Incorporating bookkeeping services can help ensure that you maintain accurate financial records and stay compliant with tax requirements. Bookkeepers can assist with the timely filing of necessary documents and ensure that your records align with legal standards.

3. Implement Robust Record-Keeping Systems

Small businesses should invest in effective record-keeping systems that make it easy to track financial data, tax filings, employee information, and other essential documents. Utilizing digital tools or cloud-based systems for document management will help ensure that records are organized, easily accessible, and secure.

Pro Tip: By using tax planning services, businesses can optimize their financial strategies to ensure compliance with tax regulations. These services can help you manage deductions, credits, and tax filings in a way that minimizes legal risks.

4. Hire Professionals to Manage Tax Compliance

Navigating the complexities of tax compliance can be overwhelming for small business owners. Hiring a professional accountant or working with a tax planning service ensures that your business remains compliant with tax laws, reducing the risk of errors or penalties.

Pro Tip: Partnering with an accounting professional who specializes in tax regulations can help small businesses maximize tax benefits, avoid mistakes, and stay on top of their filing obligations. This can also free up time for business owners to focus on growth and operational goals.

5. Provide Employee Training on Compliance Requirements

To manage employee compliance effectively, small businesses should offer regular training sessions on labor laws, workplace safety, and other relevant regulations. Ensuring that employees understand their rights and responsibilities can prevent legal disputes and foster a culture of compliance within the business.

Pro Tip: Incorporating bookkeeping services can help ensure that employee payroll is processed correctly and that all employment-related taxes and contributions are compliant with legal requirements.

6. Utilize Technology to Streamline Compliance

Technology can play a significant role in improving compliance management. From automated tax reporting tools to HR management platforms, there are various solutions that can streamline regulatory processes and reduce the time spent on manual compliance tasks.

Pro Tip: By adopting digital tools for accounting, payroll, and tax planning, small businesses can improve efficiency and ensure timely, accurate compliance with regulations.

Conclusion: Navigating Regulatory Compliance for Business Success

Regulatory compliance is a critical component of running a successful small business. While the complexities of laws and regulations can be challenging, the right strategies, tools, and professional support can help your business navigate these obstacles effectively. By staying informed, leveraging industry-specific resources, and maintaining accurate records, small businesses can ensure compliance and avoid costly legal risks.

Integrating accounting services, bookkeeping services, and tax planning services into your compliance strategy will not only reduce the administrative burden but also help your business stay on track with financial and regulatory obligations. Just as addressing technology adoption barriers and cash flow management challenges is vital for small business growth, so too is ensuring regulatory compliance.

With the right approach to compliance, your business can minimize risks, avoid legal complications, and focus on achieving long-term success.

Cash flow is the lifeblood of any small business. Without proper cash flow management, businesses can struggle to cover expenses, pay employees, and invest in growth opportunities. Unfortunately, cash flow challenges are one of the most common financial issues small businesses face, and they often lead to operational struggles, decreased profitability, and even business closures.

In this article, we’ll discuss the common cash flow management challenges small businesses experience and provide practical solutions to overcome these obstacles. Furthermore, we’ll explain how integrating accounting services, bookkeeping services, and tax planning services can help alleviate these challenges, ultimately improving your business’s financial health.

If you’ve previously dealt with marketing strategy difficulties, you may already understand how cash flow issues can affect the execution of marketing campaigns and employee retention strategies. Efficient cash flow management is crucial for addressing these and ensuring long-term business success.

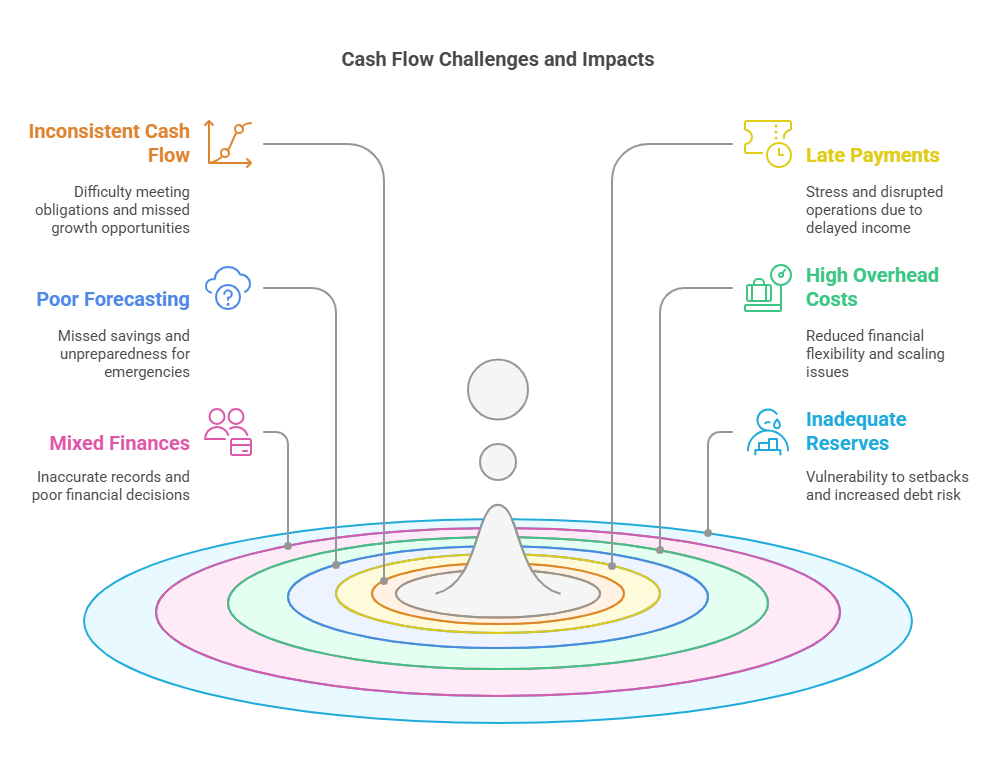

Common Cash Flow Management Challenges for Small Businesses

While every small business is unique, several recurring cash flow management challenges are common across industries. Identifying these obstacles early is the first step to ensuring a business can weather financial challenges without sacrificing growth potential.

1. Inconsistent Cash Flow

One of the most significant challenges small businesses face is irregular cash flow. For businesses that rely on sales or client payments, the timing of cash inflows often fluctuates. Seasonality, delayed payments from customers, and unexpected expenses can all contribute to inconsistent cash flow.

Impact on the Business: Inconsistent cash flow can make it difficult to meet regular financial obligations, such as paying bills or employees on time. It can also lead to missed growth opportunities, as businesses may be unable to invest in new projects or initiatives due to cash flow gaps.

2. Late Payments from Clients

Late payments from clients can create significant cash flow issues, particularly for small businesses with limited financial resources. Businesses often have to wait for overdue invoices to be paid before they can cover operational costs, and this delay can hurt their ability to function smoothly.

Impact on the Business: Late payments can cause stress for small businesses as they scramble to meet financial obligations. This disrupts operations and may force businesses to delay important decisions or investments. Furthermore, depending on customer relationships, late payments can damage client trust and harm long-term partnerships.

3. Poor Financial Forecasting and Planning

Accurate financial forecasting is critical for cash flow management. Many small businesses struggle to forecast cash flow effectively due to a lack of financial data, poor record-keeping, or ineffective financial systems. Without accurate forecasts, businesses may find themselves underprepared for fluctuations in cash flow or unforeseen expenses.

Impact on the Business: Without proper forecasting and planning, businesses may miss opportunities to save or invest when cash is available. They may also struggle to handle emergencies, such as unexpected expenses or drops in sales, leaving them unprepared for cash flow gaps.

4. High Overhead Costs

Small businesses with high overhead costs often find it difficult to maintain healthy cash flow. Regular operating expenses, such as rent, utilities, and salaries, can put pressure on cash reserves, especially when sales are inconsistent or customer payments are delayed.

Impact on the Business: High overhead costs reduce the flexibility a business has in managing its finances. Businesses may struggle to scale or pivot in response to market changes because they are tied to expensive fixed costs that don’t vary with revenue.

5. Inability to Separate Business and Personal Finances

Many small business owners mix their personal and business finances, which can complicate cash flow management. When business and personal expenses are intertwined, it becomes difficult to track the financial health of the business accurately and make informed decisions about spending and saving.

Impact on the Business: Mixing personal and business finances can lead to inaccurate financial records and tax issues. This lack of separation can also cause the business owner to make decisions based on inaccurate cash flow data, affecting the ability to invest in the business’s future or cover essential expenses.

6. Inadequate Cash Reserves

Having a safety net in the form of cash reserves is essential for small businesses. However, many small businesses lack sufficient reserves, leaving them vulnerable to unexpected financial setbacks or emergencies.

Impact on the Business: Without an adequate cash buffer, businesses are more likely to struggle when faced with unexpected costs or slower sales periods. This can lead to increased reliance on credit or loans, which can further strain cash flow and increase the risk of debt.

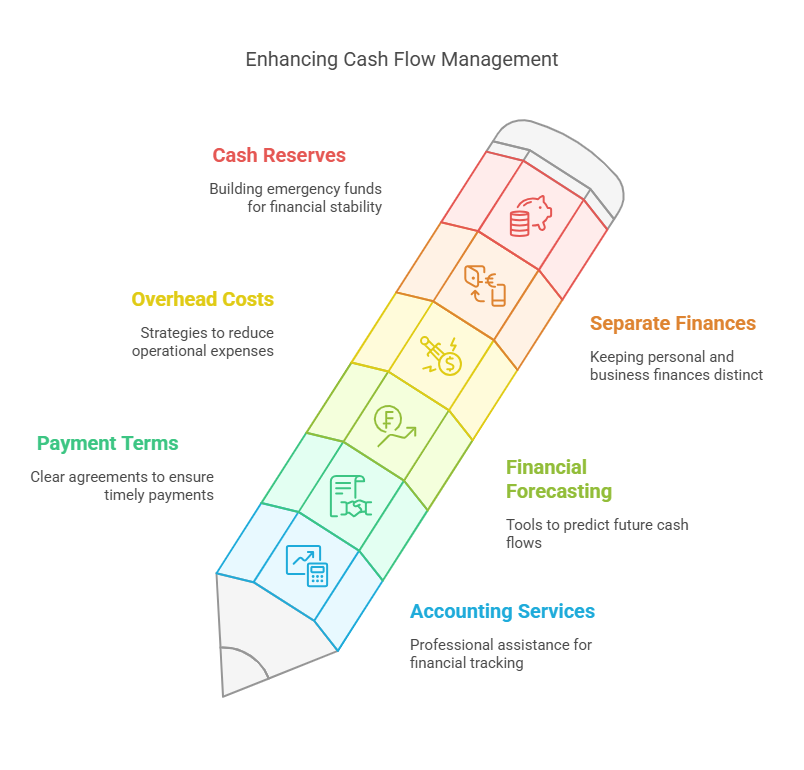

Solutions to Overcome Cash Flow Management Challenges

Now that we’ve covered some of the most common cash flow challenges small businesses face, let’s look at practical solutions that can help you manage your cash flow more effectively. These strategies are designed to minimize cash flow gaps, improve financial forecasting, and provide greater flexibility for your business.

1. Use Accounting Services for Accurate Financial Tracking

Hiring an accounting service can significantly improve cash flow management. Accounting professionals can help small businesses track their financial records, create accurate cash flow statements, and identify trends that may impact cash flow. They also ensure that taxes are filed correctly and on time, reducing the likelihood of penalties that can affect cash flow.

Pro Tip: Outsourcing accounting services enables you to focus on growing your business rather than worrying about bookkeeping. With accurate records, you’ll be able to make informed decisions on how to manage cash flow more effectively.

2. Set Clear Payment Terms and Follow Up on Late Invoices

To avoid cash flow problems caused by late payments, establish clear payment terms with clients from the outset. Be specific about payment deadlines, and enforce these deadlines consistently. If payments are overdue, follow up promptly and professionally to ensure timely payment.

Pro Tip: Consider offering discounts for early payments or charging interest on late payments to encourage clients to pay on time. Clear communication about payment terms reduces confusion and helps maintain healthy cash flow.

3. Improve Financial Forecasting and Planning

Invest in financial forecasting and planning tools that help you project future cash flows based on sales forecasts, anticipated expenses, and seasonal fluctuations. Regularly review and update these projections to account for changes in the business environment, allowing you to stay on top of potential cash flow challenges.

Pro Tip: Use bookkeeping services to generate real-time reports that help you understand the financial position of your business. By forecasting accurately, you’ll be better prepared for slow periods and more equipped to handle unexpected expenses.

4. Reduce Overhead Costs

Take a close look at your business’s overhead costs and look for areas where you can cut back or streamline operations. Whether it’s renegotiating supplier contracts, reducing utility expenses, or outsourcing non-essential tasks, reducing overhead can free up cash flow for more important investments.

Pro Tip: By utilizing tax planning services, you may be able to identify potential savings opportunities in areas such as deductions or credits. Lowering your tax burden can directly improve cash flow and leave more money available for reinvestment in your business.

5. Separate Personal and Business Finances

One of the best ways to improve cash flow management is by keeping personal and business finances separate. This will help you get a clearer picture of the business’s financial health, track expenses more accurately, and avoid potential tax issues.

Pro Tip: Working with an accounting professional ensures that your business finances are properly structured, and you’ll have a better understanding of your cash flow. Proper accounting practices also prepare you for tax season and ensure you’re maximizing deductions.

6. Build Cash Reserves for Emergencies

A healthy cash reserve acts as a buffer for times when cash flow is inconsistent. Aim to build an emergency fund that covers at least 3 to 6 months of operational expenses. This will give you the flexibility to handle downturns without resorting to loans or credit.

Pro Tip: Tax planning services can help you identify ways to optimize your profits, which can be directed into a cash reserve. By minimizing your tax liability, you free up more cash for saving and investing in your business.

Conclusion: Ensuring Business Continuity Through Strong Cash Flow Management

Cash flow is essential for business survival and growth. By addressing the common cash flow management challenges that small businesses face, you can create a more stable and sustainable financial foundation. Outsourcing accounting services, utilizing bookkeeping services, and engaging in proactive tax planning services can significantly improve your cash flow management efforts.

Just as tackling marketing strategy difficulties can help improve customer acquisition and retention, addressing cash flow challenges ensures your business has the financial resources to implement and execute these strategies effectively. With the right approach, your business will not only overcome cash flow hurdles but also set the stage for long-term success.

Creating an effective marketing strategy is essential for any business, especially small businesses striving to increase brand awareness, attract new customers, and grow their revenue. However, small businesses often face significant difficulties in developing and executing successful marketing strategies. With limited resources and competing priorities, overcoming these challenges can feel overwhelming.

In this article, we will explore the common marketing strategy difficulties faced by small businesses and provide actionable solutions. Moreover, we’ll highlight how integrating accounting services, bookkeeping services, and tax planning services can support your marketing efforts, ensuring that your business operates smoothly while tackling these challenges head-on.

If you are also struggling with employee retention issues, you’ll find that an effective marketing strategy can help your business build a stronger employer brand, attracting and retaining top talent.

Marketing Strategy Difficulties: Common Challenges Small Businesses Face

Marketing strategy difficulties are not unique to small businesses, but these companies often face additional constraints due to their size and limited budgets. Let’s dive into the most common challenges small businesses encounter when developing their marketing strategies.

1. Limited Budget and Resources

One of the primary challenges small businesses face is limited marketing budgets. With fewer resources available, it’s difficult to compete with larger competitors who can invest heavily in advertising and brand building. As a result, small businesses often feel like their marketing efforts aren’t yielding the desired results.

Impact on the Business: Limited resources can restrict the scope of marketing campaigns, reduce the frequency of content creation, and hinder the ability to track and optimize performance effectively.

2. Difficulty Defining the Target Audience

Identifying and understanding the target audience is a critical aspect of any marketing strategy. Small businesses often struggle with defining their ideal customer, leading to marketing campaigns that miss the mark or lack focus.

Impact on the Business: Failing to identify a clear target audience can lead to ineffective marketing efforts, wasted budget, and missed opportunities to engage with potential customers who would benefit from the product or service.

3. Lack of Expertise in Digital Marketing

In today’s digital age, small businesses must have a strong online presence. However, many small business owners or marketing teams lack expertise in digital marketing, making it difficult to effectively leverage digital platforms, SEO, social media, and email marketing.

Impact on the Business: Without proper knowledge of digital marketing strategies, small businesses risk falling behind in their industry. Inefficient digital marketing efforts can lead to poor results, reduced visibility, and a lack of customer engagement.

4. Ineffective Tracking and Analytics

To evaluate the success of marketing campaigns, small businesses need to track metrics such as ROI, website traffic, conversions, and engagement. However, many small businesses either lack the tools or the expertise to track these metrics accurately, making it challenging to optimize campaigns for better performance.

Impact on the Business: Without effective tracking and analytics, businesses may fail to understand which marketing strategies are working and which ones are not. This can result in spending more money on ineffective campaigns and missing out on opportunities to optimize marketing efforts.

5. Inconsistent Branding and Messaging

A lack of consistency in branding and messaging can confuse potential customers and weaken a business’s presence in the marketplace. Small businesses may struggle with creating a cohesive brand identity, which impacts customer trust and recognition.

Impact on the Business: Inconsistent messaging leads to a fragmented brand image, confusing potential customers and damaging brand credibility. This could result in lower customer retention and poor marketing effectiveness.

6. Competitor Challenges

Small businesses often face intense competition, not just from other small companies, but also from larger, established brands. Competing against larger businesses with greater resources and marketing budgets can be discouraging, making it hard for small businesses to stand out.

Impact on the Business: If a small business fails to differentiate itself from the competition, it will struggle to capture the attention of potential customers and may lose market share to larger competitors.

How to Overcome Marketing Strategy Difficulties: Practical Solutions for Small Businesses

While marketing strategy difficulties are common, they are not insurmountable. Here are several actionable solutions that can help small businesses overcome these challenges and create a successful marketing strategy.

1. Prioritize and Optimize Your Marketing Budget

Instead of spreading your budget too thin across multiple marketing channels, focus on the ones that provide the best return on investment. Consider low-cost but effective strategies like content marketing, social media marketing, and email marketing. Allocate your resources wisely, and consider outsourcing certain tasks (e.g., SEO, digital ads) to experts when necessary.

Pro Tip: Integrating accounting services can help small businesses better manage their marketing budgets by providing real-time financial insights. By understanding cash flow and expenses, businesses can make informed decisions about where to allocate marketing resources effectively.

2. Conduct Market Research and Define Your Target Audience

To develop a more effective marketing strategy, it’s essential to clearly define your target audience. Conduct market research to understand your potential customers’ pain points, needs, preferences, and behaviors. Creating buyer personas can also help narrow down your focus.

Pro Tip: Accounting services can be valuable in identifying high-value customers based on financial transactions and purchasing trends. Understanding your customer’s spending habits can give you deeper insights into their preferences and improve marketing targeting.

3. Invest in Digital Marketing Training or Experts

If your business lacks digital marketing expertise, consider investing in training or hiring professionals who can help you. Whether it’s hiring a digital marketing agency or attending online courses, gaining the skills needed to run effective digital campaigns will pay off in the long run.

Pro Tip: Utilizing bookkeeping services can help streamline business operations, leaving more time for you to focus on marketing. This allows you to implement your marketing strategies more effectively without getting bogged down by financial management tasks.

4. Use Analytics Tools to Measure Success

To make informed marketing decisions, you need to measure the performance of your campaigns. Use tools like Google Analytics, social media insights, and email marketing metrics to track the effectiveness of your marketing efforts.

Pro Tip: With tax planning services, businesses can optimize their financial strategies to ensure they have enough budget for data-driven marketing tools. Tax-efficient strategies can free up funds to invest in advanced tracking and analytics platforms.

5. Build a Consistent Brand Identity

To create a strong and recognizable brand, ensure that your business maintains consistent branding across all marketing channels. From logo design to messaging, consistency is key to building customer trust and recognition.

Pro Tip: Incorporating accounting and financial transparency through regular reports and disclosures can build trust with customers. A business that is financially stable and transparent is more likely to gain customer confidence, enhancing the overall brand identity.

6. Differentiate Your Business from Competitors

One of the most effective ways to stand out is by differentiating your business. Offer unique products, services, or features that your competitors don’t. Highlight these unique selling propositions (USPs) in your marketing campaigns to attract customers.

Pro Tip: With the help of tax planning services, small businesses can optimize their pricing strategies to stay competitive while remaining financially sound. By analyzing tax implications, businesses can adjust their pricing to attract customers without compromising profitability.

Linking Marketing Strategy to Employee Retention: Creating a Strong Employer Brand

A solid marketing strategy doesn’t just attract customers; it can also enhance employee retention. A strong marketing strategy that communicates your business values, mission, and culture will attract employees who align with those ideals. This makes it easier to retain your top talent and build a positive reputation as an employer.

By addressing both marketing strategy difficulties and employee retention issues in tandem, small businesses can not only attract and retain customers but also foster a loyal and engaged workforce.

Conclusion: Addressing Marketing Strategy Difficulties for Long-Term Success

Small businesses face several marketing strategy challenges, but by addressing them head-on and implementing practical solutions, these challenges can be overcome. From optimizing marketing budgets and defining your target audience to investing in digital marketing expertise and using analytics tools, there are many ways to improve your marketing efforts.

Integrating accounting services, bookkeeping services, and tax planning services into your business operations will support your marketing efforts by providing financial clarity and allowing you to allocate resources effectively. With these strategies in place, your business will not only improve its marketing strategy but will also be better equipped to overcome employee retention challenges and achieve long-term success.

Employee retention is a critical issue for many small businesses, especially in today’s competitive job market. When employees leave, businesses not only face the cost of hiring and training replacements but also suffer from lost productivity and lower morale within the team. Unfortunately, small businesses often face unique challenges in retaining their top talent, from limited resources to high turnover rates.

In this article, we’ll explore the common employee retention issues faced by small businesses and offer practical solutions that can help improve retention, fostering a loyal and engaged workforce. By integrating these strategies with effective accounting, bookkeeping, and tax planning services, small businesses can ensure that they not only retain employees but also maintain strong financial health.

What Are the Key Employee Retention Issues?

Before diving into the solutions, it’s important to understand the common reasons why small businesses struggle with employee retention. Let’s look at the main retention challenges and their underlying causes:

1. Inadequate Compensation and Benefits

One of the most straightforward reasons employees leave is because they feel they are not being compensated fairly for their skills and contributions. Small businesses may struggle to offer salaries that match those of larger competitors, which can lead to dissatisfaction and, eventually, turnover.

Impact on the Business: Inadequate compensation can lead to high turnover rates, which in turn can result in significant recruiting and training costs. The loss of skilled employees also impacts productivity and the business’s overall performance.

2. Lack of Career Growth Opportunities

Employees who feel stuck in their current roles, with no opportunity for advancement, are more likely to leave. Career growth is essential for employee satisfaction and long-term retention. Small businesses sometimes fail to provide clear paths for career development, especially when resources are limited.

Impact on the Business: Lack of growth opportunities can lead to disengagement and a sense of stagnation among employees. This often results in lower morale, decreased productivity, and higher turnover rates.

3. Poor Work-Life Balance

Work-life balance has become a key factor in employee retention. Small businesses often have fewer resources to offer flexible working hours or remote work options, making it harder for them to compete with larger companies that provide such benefits.

Impact on the Business: Employees who struggle to balance work with personal life often experience burnout, leading to disengagement and, eventually, resignation. Offering flexibility where possible can enhance retention by fostering a healthy work-life balance.

4. Lack of Recognition and Appreciation

Employees who feel their hard work is not appreciated are more likely to leave for a company that values their contributions. Recognition doesn’t always have to be monetary—it can come in the form of praise, awards, or other non-financial incentives.

Impact on the Business: When employees don’t feel valued, their productivity can drop, and they may lose their motivation to contribute. This leads to poor employee engagement and higher turnover.

5. Unclear Job Expectations and Lack of Support

Small businesses often lack the systems and structures to properly onboard and train employees, leading to confusion around job expectations. Employees who are unsure of their roles or feel unsupported in their work are more likely to leave.

Impact on the Business: Unclear job roles and inadequate support can cause frustration and uncertainty, leading to poor performance and increased turnover. Onboarding programs and clear communication can help mitigate this issue.

How Can Small Businesses Overcome Employee Retention Issues?

Addressing these common employee retention issues requires a multifaceted approach. Small businesses can implement the following strategies to improve retention and ensure they keep their top talent.

1. Offer Competitive Compensation and Benefits

While small businesses may not be able to match the salaries of larger corporations, they can still offer competitive compensation packages that align with industry standards. Additionally, benefits such as health insurance, retirement plans, and performance bonuses can significantly enhance employee satisfaction.

Pro Tip: Small businesses can also offer unique benefits that larger companies might not, such as more flexible working arrangements, casual work environments, or the opportunity to take on diverse roles and responsibilities. These benefits can add significant value to the employee experience.

2. Implement Career Development Programs

Providing employees with opportunities to develop their skills and advance in their careers is key to retaining top talent. Small businesses can invest in training programs, mentorship opportunities, and regular performance reviews to help employees grow within the company.

Pro Tip: Encourage employees to pursue relevant certifications, attend workshops, or take part in online courses. Not only does this contribute to career growth, but it also benefits the business by enhancing the skills of the workforce.

3. Prioritize Work-Life Balance

Offering flexible work arrangements, such as remote work options or flexible hours, can significantly improve employee retention. Small businesses can also foster a culture that encourages employees to take breaks, use their vacation time, and avoid excessive overtime.

Pro Tip: Implementing policies that prioritize employee well-being and offering work-from-home options, where feasible, can go a long way in enhancing retention and reducing burnout.

4. Foster a Culture of Recognition and Appreciation

Employees who feel appreciated are more likely to stay with a company. Small businesses can implement low-cost, high-impact recognition programs, such as employee of the month awards, personalized thank-you notes, or small tokens of appreciation.

Pro Tip: Publicly recognize employees for their accomplishments during meetings or through internal communications. This builds morale and motivates others to excel.

5. Improve Onboarding and Training Processes

A smooth and comprehensive onboarding process can make a significant difference in employee retention. Ensure that new hires have clear expectations and receive the support they need to succeed in their roles. Ongoing training and development are also crucial for employee satisfaction.

Pro Tip: Invest in efficient onboarding programs and offer mentorship opportunities to new hires. This creates a sense of belonging and helps employees feel confident in their roles from the start.

6. Use Accounting and Bookkeeping Services to Streamline Financial Management

Small businesses can use accounting services to better manage their budgets and cash flow, which in turn helps them allocate resources for employee retention efforts. Bookkeeping services can ensure that your financial records are up to date, allowing you to make informed decisions about employee compensation and benefits.

Pro Tip: Outsourcing accounting and bookkeeping services can help you save time and reduce the risk of errors, freeing up resources that can be reinvested in employee retention strategies.

7. Leverage Tax Planning Services for Financial Efficiency

Tax planning services can help small businesses optimize their financial strategies, ensuring that they can allocate funds to employee programs without negatively impacting their bottom line. By taking advantage of tax-saving opportunities, businesses can improve their financial health and offer better compensation and benefits to employees.

Pro Tip: Consulting with a tax planning service can help you identify tax credits, deductions, and other opportunities to reduce your tax liability, giving you more financial flexibility to invest in employee retention.

Conclusion: Retain Your Top Talent and Ensure Long-Term Success

Employee retention is a critical challenge for small businesses, but with the right strategies in place, it’s possible to overcome these obstacles. By offering competitive compensation, fostering career growth, promoting work-life balance, and improving recognition, small businesses can build a loyal and engaged workforce.

Incorporating accounting, bookkeeping, and tax planning services into your business operations can also help streamline your financial processes, giving you the resources needed to support these retention strategies. With the right approach, you can retain top talent, reduce turnover costs, and set your business up for long-term success.

For small businesses looking to improve employee retention and streamline their financial management, it’s essential to consider how accounting services, bookkeeping services, and tax planning services can play a vital role in supporting these efforts. Don’t let employee turnover impact your business—take proactive steps to foster a loyal, motivated workforce.

Managing cash flow is one of the most critical aspects of running a successful small business. Effective cash flow management ensures that your business has enough funds to cover expenses, invest in growth, and weather financial challenges. Here are some top cash flow tips for small business owners to help maintain a healthy financial position:

1. Monitor Cash Flow Regularly

Regularly tracking your cash flow is essential. Use accounting software or a simple spreadsheet to record all inflows and outflows of cash. This will help you understand your cash position at any given time and identify trends or issues early.

2. Maintain a Cash Reserve

Having a cash reserve can provide a buffer during lean periods or unexpected expenses. Aim to set aside enough to cover at least three to six months of operating expenses. This will give you peace of mind and the flexibility to navigate through tough times.

3. Optimize Inventory Management

Inventory can tie up a significant amount of cash. Implementing an efficient inventory management system helps reduce excess stock and minimizes holding costs. Regularly review your inventory levels and adjust orders based on demand to free up cash.

4. Invoice Promptly and Follow Up

Timely invoicing is crucial for maintaining cash flow. Send out invoices as soon as a product or service is delivered, and follow up on overdue payments. Consider using automated invoicing and payment reminders to streamline the process.

5. Negotiate Payment Terms

Negotiating favorable payment terms with suppliers can improve your cash flow. Aim for extended payment terms to give yourself more time to pay. Conversely, if possible, offer discounts to customers for early payments to accelerate receivables.

6. Control Operating Expenses

Regularly review your operating expenses and identify areas where you can cut costs. Look for non-essential expenses that can be reduced or eliminated. This could include renegotiating contracts, finding more cost-effective suppliers, or reducing overhead costs.

7. Offer Flexible Payment Options

Providing flexible payment options can encourage quicker payments from customers. Consider accepting credit cards, electronic payments, and offering installment plans. The easier it is for customers to pay, the faster you’ll receive cash.

8. Manage Debt Wisely

While taking on debt can be necessary for growth, it’s important to manage it wisely. Avoid over-leveraging and ensure you can comfortably meet debt repayments. Consider refinancing high-interest debt to lower your monthly payments and improve cash flow.

9. Plan for Seasonal Variations

Many businesses experience seasonal fluctuations in cash flow. Plan ahead for these variations by building up cash reserves during peak seasons and reducing expenses during slower periods. This will help you maintain stability throughout the year.

10. Seek Professional Advice

Sometimes, managing cash flow can be challenging, and seeking professional advice can make a significant difference. An accountant or financial advisor can provide valuable insights and strategies tailored to your specific business needs.

Conclusion

Effective cash flow management is vital for the sustainability and growth of your small business. By implementing these tips, you can ensure a steady flow of cash, reduce financial stress, and position your business for long-term success. Remember, the key to successful cash flow management is regular monitoring, strategic planning, and proactive decision-making.